The role of the car is changing as consumers opt for pay-on-use services as an alternative to ownership in congested cities. Suppliers and manufacturers will have to adapt their strategies as a result, argues Sampo Hietanen, chief executive officer and founder of mobility company MaaS Global.

Cars are magical. And now I do not refer to people’s obsession with speed, contours, mechanics and power. I am referring to value creation.

Just about all other modes of transport are practical investments - trains, buses, trams, trucks, electric scooters - but with a car you are not just paying for the output, getting from one place to another; you are paying to be who you want to be, how you want to feel and how you want to be seen.

That’s the magic. A carmaker takes a heap of metal and plastics and turns it into a building block of a client’s identity.

But now this is in flux. Urban congestion, climate change and the sharing economy powered by digital platforms are all making people reconsider the benefits of owning a car.

Yet this is just tremor before the real earthquake; when totally autonomous, self-driving cars hit the streets, private automobile ownership will go into free fall. How will the massive automobile industry, the symbol of modernism and progress, react to this?

If people do not own the cars, who will? Before we try to answer that, let’s look at how user behaviour might change.

If you don’t own the car you use, you might not choose the dullest option available – maybe you want to experiment a bit. And you will probably choose new over old. Roads will get a lot more interesting than they are today.

Or maybe the pendulum will swing into the opposite direction; since it is not yours, you stop caring what is driving you around – it’s just a trip, so who cares.

So, if I were an automaker, I’d be pondering the following questions night and day.

Once people stop owning cars and start using them as a service:

- Will they go for new and interesting, or will cars become a commodity?

- Who’s going to own the cars - automakers or service providers?

- What will be the role of service - will it become the differentiating factor and focus of innovation?

There are no sure-fire answers available, but I have a hunch about how it will play out.

Carmakers will want to hold on to their margins, which are in the brand value of their products. If cars become a commodity, this value will be wiped out.

As people will probably want to drive, or rather be driven, in new, comfortable and interesting cars, the automakers will compete based on their brand attributes.

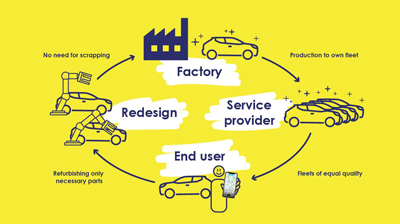

Since the carmakers’ business model is no longer focused on selling a new car, and they don’t need to worry about the customer carrying the burden of it getting old, they will start making cars that don’t age.

They will decide to own the cars they make and build them so that they can be updated and upgraded forever.

Therefore, the scrapping business will almost disappear when cars stay on the road forever. Parts will be changed as they age and new features added when they are developed.

This will be a circular economy like you’ve never seen before!

The alternative is that the service providers will own the cars. Then, they set the requirements for the cars they want and the automakers will simply become factories pushing out white-label automobiles. This is possible but unlikely. Daimler, BMW or Toyota will not voluntarily become slaves to the service providers.

The concentration of vehicle ownership is something that regulators will love.

Instead of there being hundreds of millions of car owners who all have an opinion on every little detail, there will be a dozen or two carmakers who own fleets that can be upgraded or tweaked at will, or rather at the regulator’s will.

Governments can impose restrictions, requirements and tax breaks that will have almost immediate effects.

And how does the developing Mobility-as-a-Service ecosystem fit into this? Perfectly well.

Most people are already living in cities and their number is growing fast. In cities, public transportation, bikes, scooters and walking are popular, particularly as it gets more crowded.

Using a car to get around will be an exception, reserved for moving heavy goods, going beyond city limits for a weekend or wanting to impress someone.

Cars, probably owned by their makers, will be offered as part of comprehensive Mobility-as-a-Service packages. The day-to-day service to customers will be handled by those concentrating on customer experience, not by those concentrating on manufacturing.

The way I see it, in the future the innovations and the value creation, as well as the customer, will be shared by the carmaker and the service provider.

From this perspective, as an operator in the service layer, I would like the auto industry to work hard on the following issues.

- Build close relationships with service providers, since they will be the single most important touchpoint to customers and their needs. Co-innovate.

- Focus not on how many cars you manufacture, but on how many you have on the road.

- It will not be the number of your cars, but the value of your cars that matters. By concentrating on the quantity, you regress into the commodity game.

- The most versatile automobiles get the most mileage. Can the same self-driving car be used for family entertainment, business meetings, focused intellectual work and also function as a delivery van?

To phrase it differently, if you can figure out the difference between a KIA and a Ferrari in the digital age, you’ll do just fine.

* Sampo Hietanen (pictured) is chief executive officer and founder of MaaS Global. MaaS Global is the company behind the Whim smartphone app, an all-inclusive Mobility-as-a-Service solution that gives users all city transport services in one subscription, letting them book journeys through a single smartphone app to take them where they want, on-demand, covering public transport, taxis, bikes, cars, and a range of other options. This article first appeared on the MaaS Global blog.