UK Finance & Leasing Association members report that new asset finance business grew by 9% to almost £1.7 billion in January 2014, compared with the same month last year.

Geraldine Kilkelly, head of research and chief economist at the FLA said that key asset sectors reported double digit growth - with commercial vehicle finance, business equipment finance and plant and machinery finance up by 25%, 21% and 13% respectively.

IT equipment finance reported modest new business growth of 3% compared with the same month in 2013.

Kilkelly added: “The positive start to 2014 follows exceptionally strong growth of more than a third in December 2013 and reflects growing confidence in the sector.

“The FLA’s Asset Finance Confidence Survey for Q1 2014 showed respondents expect asset finance new business to grow by up to 10% over the next 12 months.”

| Jan 2014 |

% change on

Jan 13

|

3 mths to

Jan 14

|

% change on

prev yr

|

12 mths to

Jan 14

|

% change on

prev yr

| |

|---|---|---|---|---|---|---|

| Total FLA asset finance (£m) | 1,694 | +9 | 5,705 | +14 | 22,535 | +4 |

| Total leasing and hire purchase excluding high value (£m) | 1,672 | +7 | 5,603 | +13 | 21,843 | +4 |

| Data Extracts: | ||||||

| Plant and machinery finance (£m) | 343 | +13 | 1,069 | +9 | 4,513 | +5 |

| Commercial vehicle finance (£m) | 420 | +25 | 1,504 | +38 | 5,285 | +11 |

| IT equipment finance (£m) | 68 | +3 | 412 | +13 | 1,544 | +14 |

| Business equipment finance (£m) | 159 | +21 | 493 | +12 | 1,961 | +3 |

| Car finance (£m) | 505 | -8 | 1,599 | +1 | 6,707 | -1 |

| Aircraft, ships and rolling stock finance (£m) | 6 | -62 | 115 | +42 | 297 | -40 |

Nevertheless, the fact remains that UK productivity has been declining since the onset of the financial crisis, and today the gap with G7 nations is at its widest since 1992.

This week three economists from the LSE’s Centre for Economic Performance argued that underinvestment is key to understanding this. The recovery so far seems unbalanced; and policymakers must focus on raising productivity to prevent it fizzling out.

The latest data from the Office for National Statistics (ONS) show that the UK’s productivity gap with other G7 nations is at its widest since 1992. This bad news comes against the backdrop of increased optimism as the economy seems finally to have returned to growth. Unfortunately, this growth seems to be generated by Britain’s usual suspects: consumer spending and a booming housing market (stoked by government subsidies like Help To Buy) rather than from exports and investment. The danger is that a recovery without underlying productivity growth is unsustainable.

“What is needed,” they said, “is renewed focus on raising productivity. Business investment is a crucial ingredient, and the government can do more to support this.”

Illuminating the productivity puzzle?

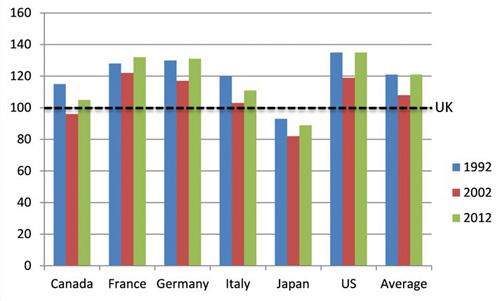

The latest ONS figures show that in 2012 labour productivity as measured by output per hour was 21% below the G7 average (Figure 1) – the widest gap for 20 years. In output per worker terms, the gap was 25%. Moreover, output per hour in 2012 was 3% lower than in 2007, a full 16% below the level it would have been on long-term pre-2007 trends continued. This lacklustre productivity performance since the financial crisis has been dubbed the “Productivity Puzzle” because such a fall has been unprecedented in post war UK history.

Output per Hour Worked, G7 Countries (UK=100)

Current price GDP per hour worked from ONS data, release date February 2014. Average refers to G7 average, excluding UK.

For many “supply side pessimists”, this indicates a large and permanent loss to productivity. According to this view output is very close to potential and so monetary and fiscal policy must be tightened.

“The flipside of the puzzle of low productivity is a jobs conundrum. Given that GDP growth has been so poor, it is remarkable that unemployment is not higher. Central to understanding this is the fact that UK real wages are far more flexible than in past recessions due to weakened union power and welfare reforms.

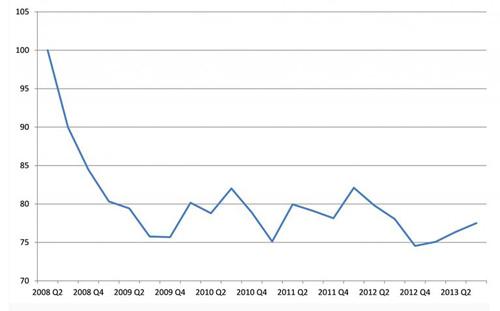

“In response to low demand, real wages have fallen by 8% since Lehman’s collapse (based on data to October 2013). This has helped keep labour costs low for employees and sustained higher employment. However, low wages and rising costs of capital due to banking dislocation have deterred business investment, as has high uncertainty and the disastrous decision to slash of public investment by half. Figure 2 shows how real investment has collapsed since 2008.”

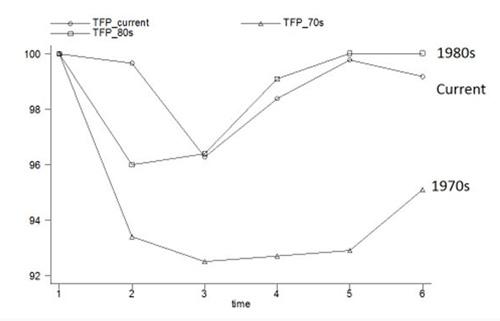

“Lower investment can depress the amount of capital per worker and so will reduce labour productivity. Less machines per employee means less output per employee. This is not a fundamental loss of efficiency – as demand improves and credit markets return to normal productivity should rebound. A close inspection of the data, reveals that once we correct labour productivity for these changes to get a measure of efficiency (sometimes called Total Factor Productivity or TFP), things are not so different this time round from other severe recessions (see Figure 3).

Other factors may also matter for the recent productivity puzzle such as misallocation of capital due to forbearance, mis-measurement of intangible capital and labour quality deterioration. But the under-utilized resources caused by low demand and “capital shallowing” due to changes in the prices of labour and capital seems to explain a large chunk of the mystery.

“The LSE Growth Commission has shown that there is underlying strength in the UK economy built up since the early 1980s when the UK reversed a century of relative economic decline. Productivity growth in the three decades leading up to the crisis was broad based with finance only contributing around a tenth of the improvement. Much of these improvements were due to policy reforms strengthening competition in product and labour markets, the benefits of which are unlikely to suddenly evaporate.”

The collapse of real investment, 2008-2012 (2008 Q2=100). Investment defined as total (cross sector) gross fixed capital formation, chained volume measures, seasonally adjusted.

ONS data, release date December 2013

Change in Total Factor Productivity across UK recessions

1970s and 1980s derived from EU KLEMS data. 1970s recession is 1973-1978; 1980s recession is 1979-1984; Current is 2007-2012. 2000s authors’ estimates in Pessoa and Van Reenen (2013)

Unbalanced recovery

Business investment has stayed flat: the latest ONS data show that while business investment rose 2% in Q3 2013 compared to the previous quarter – it was 5.3% lower than Q3 2012.

Distortions with our financial sector still remain – lending to companies has not picked up, despite favourable credit conditions and lower funding costs for banks. Banks are attempting to re-build their balance sheets which have made them reluctant to lend, and enforce covenants over bad loans. The result is insufficient capital is flowing to high growth potential enterprises.

Long term, pro-growth policies

Most of the recent falls in productivity are due to temporary factors such as weak demand and financial sector turmoil. Poor fiscal policy and a failure to adequately address banking problems has exacerbated these problems, but cannot hold back the rebound indefinitely.

This should not make us complacent over productivity. There was a significant gap with our peers even prior to the crisis (as can be seen in Figure 1) which held back living standards. We need to focus on strengthening the foundations of the UK through long-run investments in infrastructure, skills and innovation along the lines set out by the LSE Growth Commission. Cutting public investment in a depression is bad short-term macro policy as well as foolish long-term growth policy. In political terms it made sense – cuts in investment are bruises that are not usually seen in public. That is, until many years later or, in the case of flood defences, when the water starts coming down.

Note: This article gives the views of the authors, and not the position of the British Politics and Policy blog, nor of the London School of Economics.

João Paulo Pessoa is an occasional research assistant in CEP’s productivity and innovation programme. Anna Valero is in her third year of the LSE MRes/PhD in Economics, and works on the Productivity and Innovation programme. John Van Reenen is Professor in the Department of Economics London School of Economics and the Director Centre for Economic Performance, London School of Economics. He is also Fellow of the British Academy, Econometric Society and the Society of Labour Economists.